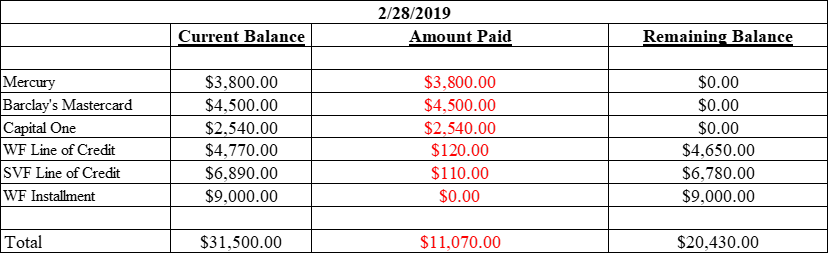

At the end of February, all my credit cards have been paid to zero. After discussion with my wife, and explaining the benefits of the installment loan, I got a $9,000 installment loan, and used $1,840 which is a combination of my normal debt reduction payments plus an extra amount to pay all my credit cards to zero. This moment is the 1st since my early 20’s that I’ve been able to pay my credit card debt to zero. I thank God for this moment, and even shared the zero balances with my wife in celebration.

In previous blog posts, I’ve talked about the benefits of using an installment loan to consolidate debt. My wife understandably had her reservations with me getting into more debt, so let me clarify the specific conditions in which using an installment loan for debt consolidation is ideal in my opinion.

- Your interest rate is going to be lower than the rate you are paying on your credit cards

-

You can have control of the term of the loan (36 months, 48 months, or 60 months)

- This control is important, because the longer the term the lower your payment will be.

- This control is important, because the longer the term the lower your payment will be.

-

There is no origination fee, or it is financed into the loan.

- If there is an origination fee, it will affect your monthly payment amount

- If there is an origination fee, it will affect your monthly payment amount

- Make sure your payment amount will be the same or lower than what you’re currently paying and when it will be to fit in your budget

In my situation there was no origination fee, the payment would be less than what I normally pay on my debt around the 15th of month, and I had enough credit card debt paid down that this would fit with my debt free plan and even accelerate it. I would recommend that you not take out multiple installment consolidate credit card debt if you don’t have the discipline to not use your credit cards and know how the installment loan payment will affect your monthly cash flow. Remember that with installment loans the payments are fixed, however installment loans may improve your credit score, because they have a different weight on to the credit bureaus vs. (credit card) open/revolving credit. Based on this re-structure, I should be able to pay off the lines of credit by the end of this year, and hopefully pay off the installment loan by next year.

If you want to learn more about how I’m increasing my income while reducing debt, or if you want to have someone to discuss your debt reduction strategy with, or if you need a financial check-up, contact me.

Also, learn more about how I use the self-lending principle through contacting me

This month’s video is The Greatest Motivational Video for Success & Gym – VALOR – 35 Minute Motivation Speeches from the Mulligan Brothers YouTube channel.

“The LORD will send rain at the proper time from his rich treasury in the heavens and will bless all the work you do. You will lend to many nations, but you will never need to borrow from them.”

Deuteronomy

28:12

NLT

http://bible.com/116/deu.28.12.nlt

I believe in your journey to….

A Debt Free Me