2018 is ending, and I’m glad this year is over with. This year has been a Year of Restoration. There’s been restoration in my finances and even more importantly restoration in my marriage. Restoration isn’t an easy process. When you think about a car being restored, there’s a lot of sweat, hard work, and physical reconstruction that can happen. Our Jack Russell Terrier, Sasha, had surgery to have two tumors removed and now she’s cancer free! There were quite a few challenges especially toward the end of the year, which increased the level of stress in our lives, but in those moments our faith increased too. When you find yourself in stressful and difficult moments, make sure to surround yourself with people who genuinely want to lift you up even if it’s emotionally. Throughout the year, and at the start of the blog, I haven’t fully disclosed all my consumer/credit card debt. I didn’t give full disclosure because I didn’t want to share how large the number was, and at the same time I didn’t want to discourage anyone from taking the steps to become debt free. Going forward I will disclose all my credit card and lines of credit debt for the purpose of being honest. I do have $25,067.91 in student loan debt, but my path to becoming debt free involves becoming debt free of credit card and lines of credit debt. My student loan is on a set income driven repayment plan and will be paid off by 2034 at a fixed rate of 3.125%. 2019 will be a year of great joy and you’ll see the remaining debt I have left to pay as I step closer to being debt free.

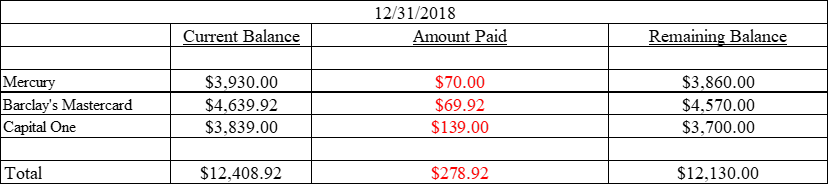

To encourage you, I started this year at $43,824.60 in credit card, revolving line of credit, and term debt combined. As of now, I’ve paid it down by $19,624.60 to $24,200.00. I was able to reduce my debt by this much by selling what I didn’t need to pay down portions of debt, consolidating multiple cash accounts, and using portions of my tax refund and bonus toward debt. I also completely focused on reducing a balance. Since the first blog post you’ll notice I don’t share the interest rate on the debt. The reason is because I want you to explore the two different debt reduction methods: the debt avalanche method and the debt snowball method. Personally, both methods work, and I’ve focused on debt based on how it makes me feel. I’ll also add that in addition to how I feel, I discuss with my wife my reason for switching to pay one debt with a lower interest versus a debt with a higher interest rate. In those scenarios, it’s because the balance is low enough that I can eliminate the debt within a shorter time frame. The second reason I don’t share the interest rate is because your debt reduction strategy is YOUR debt reduction strategy. You personally own it, must be responsible for it and most importantly be committed to following it day after day and month after month. My debt reduced when I finally committed to reducing it.

Your journey is different than mine, but we can take one step at a time together.

If you want to learn more about how I’m increasing my income while reducing debt, or if you want to have someone to discuss your debt reduction strategy with, or if you need a financial check-up, contact me.

Also, learn more about how I use the self-lending principle through Mustard Seed in the mustard seed section.

This month’s video is When You Are About To Give Up WATCH THIS! – Motivational Video Speeches 2019 from the Mulligan Brothers YouTube channel.

“The LORD will send rain at the proper time from his rich treasury in the heavens and will bless all the work you do. You will lend to many nations, but you will never need to borrow from them.”

Deuteronomy

28:12 NLT

http://bible.com/116/deu.28.12.nlt

I believe in your journey to….

A Debt Free Me